Healthcare investors, whether they be private equity firms, public companies or non-profit institutions, are always on the lookout for underdeveloped subsectors that are well-positioned for disruption, consolidation, and growth. An emerging investment theme we are seeing from some of the savviest investors in the marketplace is cropping up in primary care, particularly around care delivery models that address the industry’s biggest pain points. As evidence of this trend, this December we advised a network of nearly 30 tech-enabled primary care centers with a unique physician-focused model on its growth capital raise from a prestigious multi-billion-dollar private equity firm. Which assets within primary care are attracting the strongest interest? Following are some key attributes:

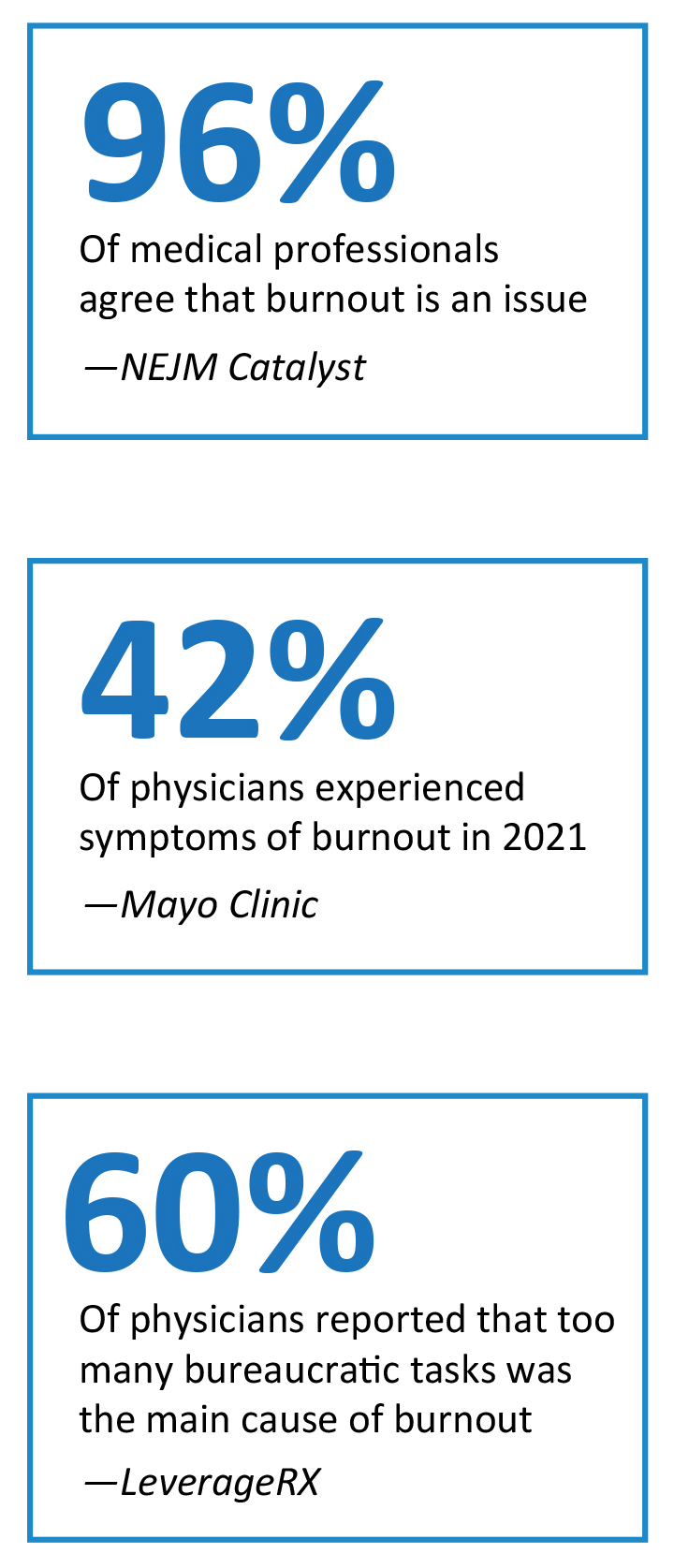

Offer a Solution to Physician Burnout

Primary care models that focus on provider satisfaction and address physician burnout to ensure great patient care are winning. Operators that empower physicians by offloading burdensome non-medical work through process improvements and technology, as well as those that increase physician agency, scheduling flexibility, and work-life balance, are being rewarded not only with higher levels of physician retention but also with significant investment interest.

Reduce Costs Relative to Hospital and Hospital System Care Delivery Models

In many states, hospital systems negotiate primary care patient visit reimbursement rates that are two or more times higher than the rate paid for in-office visits to independent or non-affiliated primary care physicians. Providers who are able to offer high-quality care without a hospital or health-system affiliation are preferred by payers and, as a result, can often see significant growth with modest marketing spend. Further, as the “gateway” to the broader healthcare system, primary care physicians can help identify high-risk patients and address health issues in a preventative manner before they become more expensive to address.

Optimize and Streamline the Patient Experience

Healthcare consumers want an amazing patient experience powered by technology solutions. Far lagging the broader retail economy, poor patient experience has plagued the primary care space for years, from “single shingle” independent physician offices all the way to large integrated health systems, whether through long wait-times for in-person visits, long hold-times for patients calling in, or time-consuming and often duplicative paperwork at admission as well as at various stops along the patient journey. Companies that can leverage technology, offshoring, and centralized management to bring efficiencies that improve the patient experience are seeing higher patient retention, driving better financial performance and increased investor interest.

Highly Fragmented Market, Primed for Consolidation

The primary care market remains ripe for investment, innovation, and consolidation. According to the AMA, there are over 220,000 active primary care physicians in the U.S. today. Nearly half of those physicians are owner operators of independent practices. While specialty practice groups have seen several waves of consolidation (which Intrepid has covered across urology, fertility, and other specialty physician practice management subsectors), consolidation in the primary care space remains in its infancy. Traditional investing playbooks taken from prior waves of specialty practice group consolidations need to be refreshed to address the unique challenges of the primary care landscape, however massive opportunities exist for those investors willing to roll up their sleeves and invest in differentiated models that meet today’s challenges head on.

Overall, we expect that healthcare investors will continue to see opportunities to disrupt the primary care space and back care delivery models with a proven ability to improve the patient experience, increase physician retention, and reduce costs for payers. Given the benefits of scale to increase efficiency and amortize technology and back office spend across more clinic locations, we believe that the next wave of consolidation in the space is only just beginning.